EXECUTIVE SUMMARY

- The era of persistently low interest rate volatility has ended, creating a more attractive environment for residential mortgage-backed securities (RMBS).

- Historically, higher volatility has been associated with stronger mortgage alpha—a relationship that may persist.

- Mortgages provide a liquid, differentiated return stream that remains underrepresented in many portfolios.

- Allocations across both agency and non-agency RMBS can enhance total return through incremental alpha.

- Increasing mortgage exposure can reduce corporate credit concentration, help maintain duration targets, and improve overall portfolio resilience.

INTRODUCTION

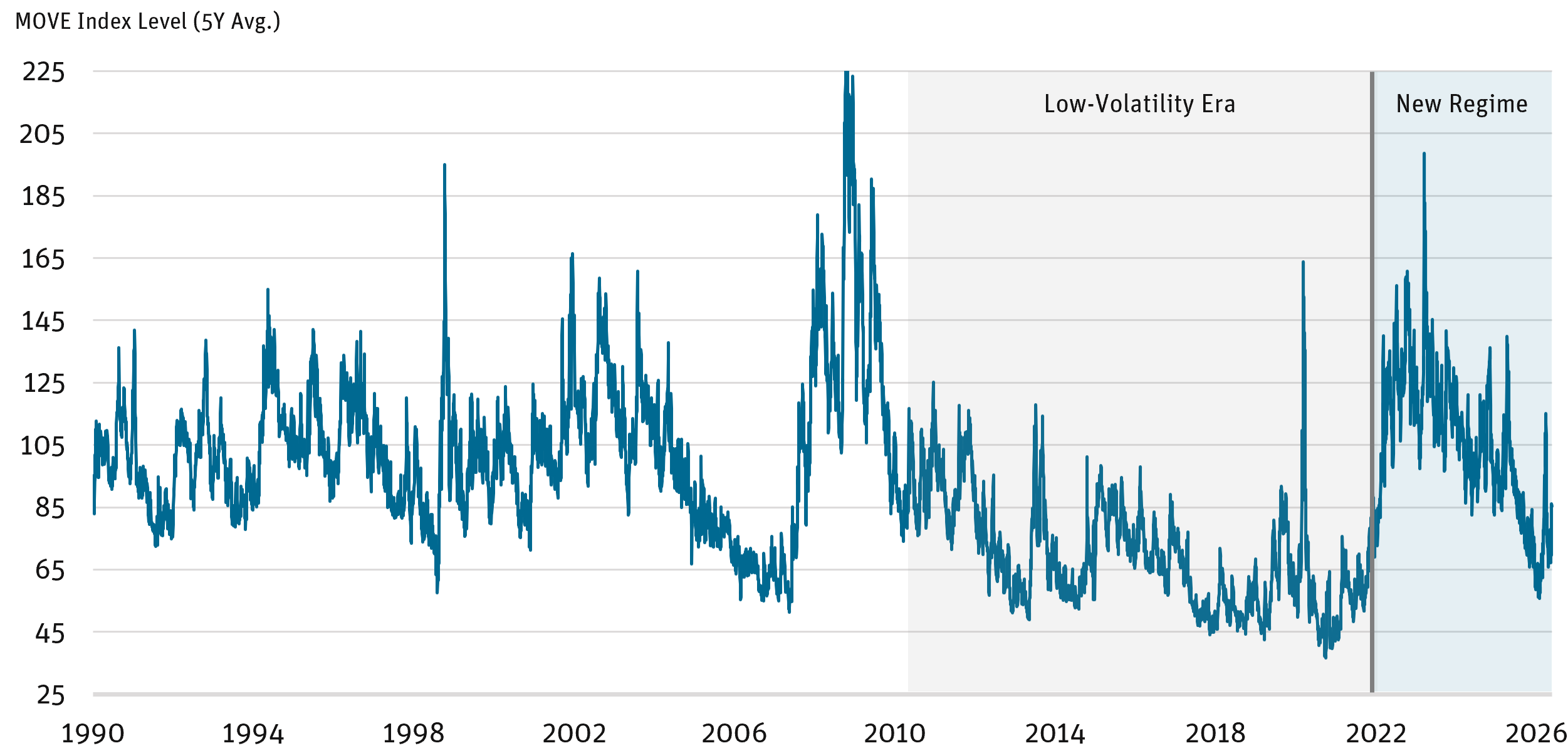

The fixed income landscape has undergone a fundamental shift as interest rate volatility has moved into a structurally higher regime (Figure 1).

Figure 1: Interest Rate Volatility Has Moved Higher

Source: Bloomberg as of 4/30/26.

Following the global financial crisis (GFC), interest rate volatility remained unusually subdued for more than a decade, suppressed by persistent deflationary pressures and the Federal Reserve’s extensive quantitative easing programs. This prolonged stability shaped investor behavior and asset allocation across fixed income.

That environment has now ended. The post-GFC volatility regime has given way to one characterized by persistently elevated interest rate volatility—with meaningful implications for agency and non-agency mortgage-backed securities (MBS), alpha generation, and portfolio construction.

FROM SUPPRESSED TO STRUCTURAL: A NEW VOLATILITY REGIME

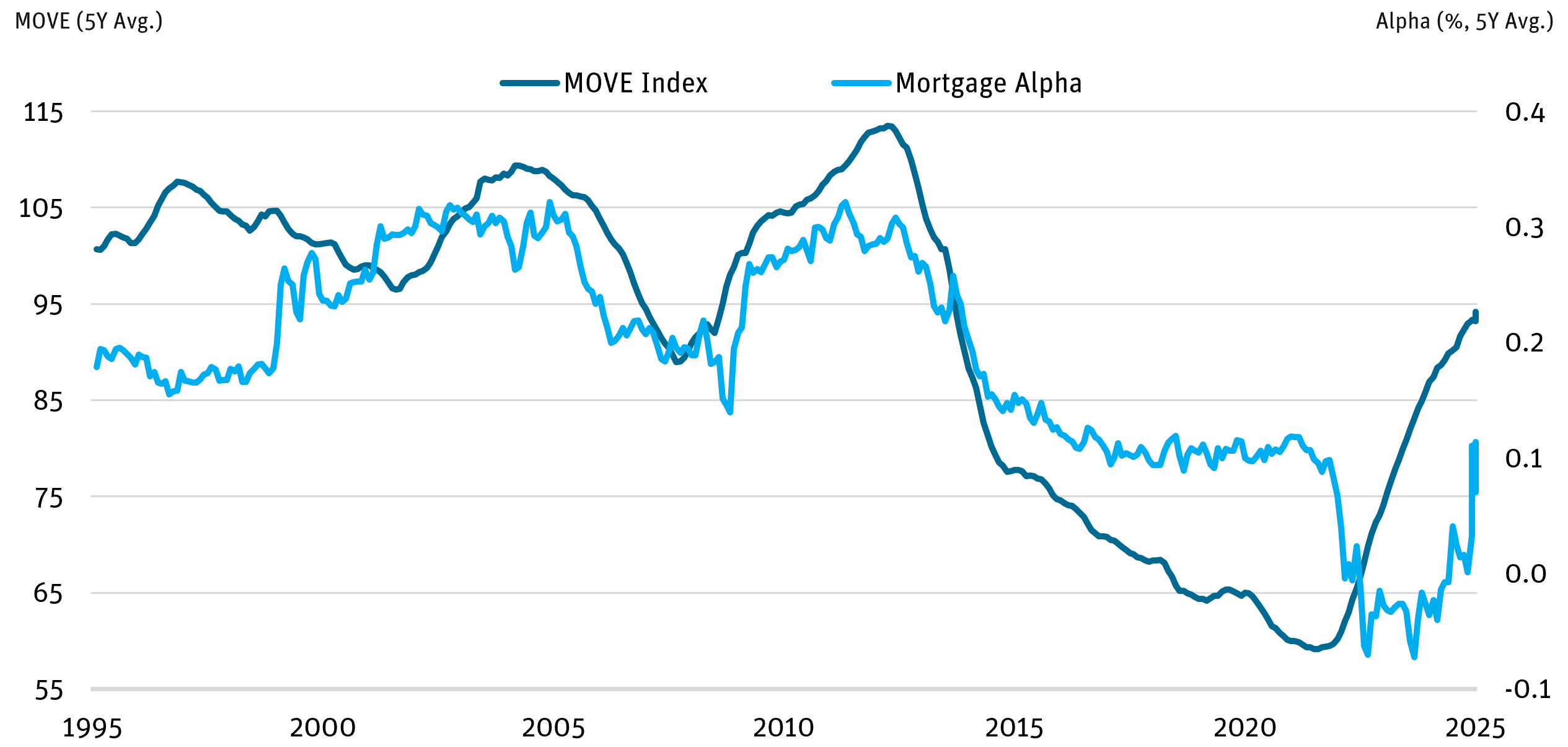

Historically, elevated volatility appeared in short bursts tied to macroeconomic shocks or policy transitions. Today’s environment, however, reflects a more structural repricing of inflation, monetary policy, and economic growth.

The MOVE Index’s rolling five-year average highlights this transition, showing a sustained increase from post-GFC lows (Figure 2). This shift is particularly important for RMBS, which are uniquely sensitive to interest rate volatility through prepayment dynamics, convexity behavior, and option-adjusted spreads.

As volatility rises, the value of embedded borrower options increases, widening spreads and creating opportunities for active managers to capture incremental yield.

Figure 2: Mortgage Alpha Increases as Interest Rate Volatility Rises

Source: Bloomberg as of 2/28/25. Data shown as five-year rolling averages. Mortgage alpha represents excess return relative to U.S. Treasuries.

MORTGAGES PROVIDE A DIFFERENTIATED SOURCE OF RETURN

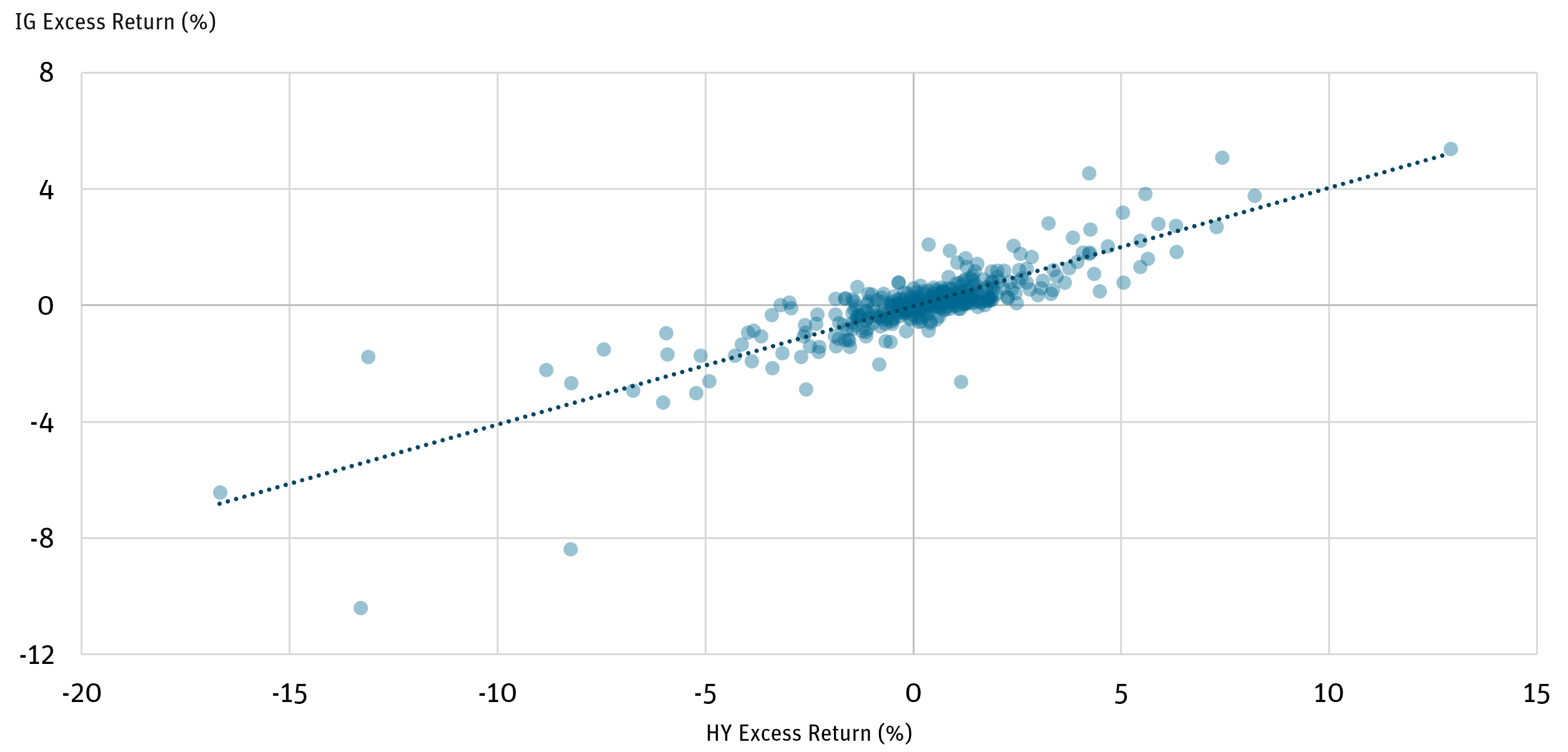

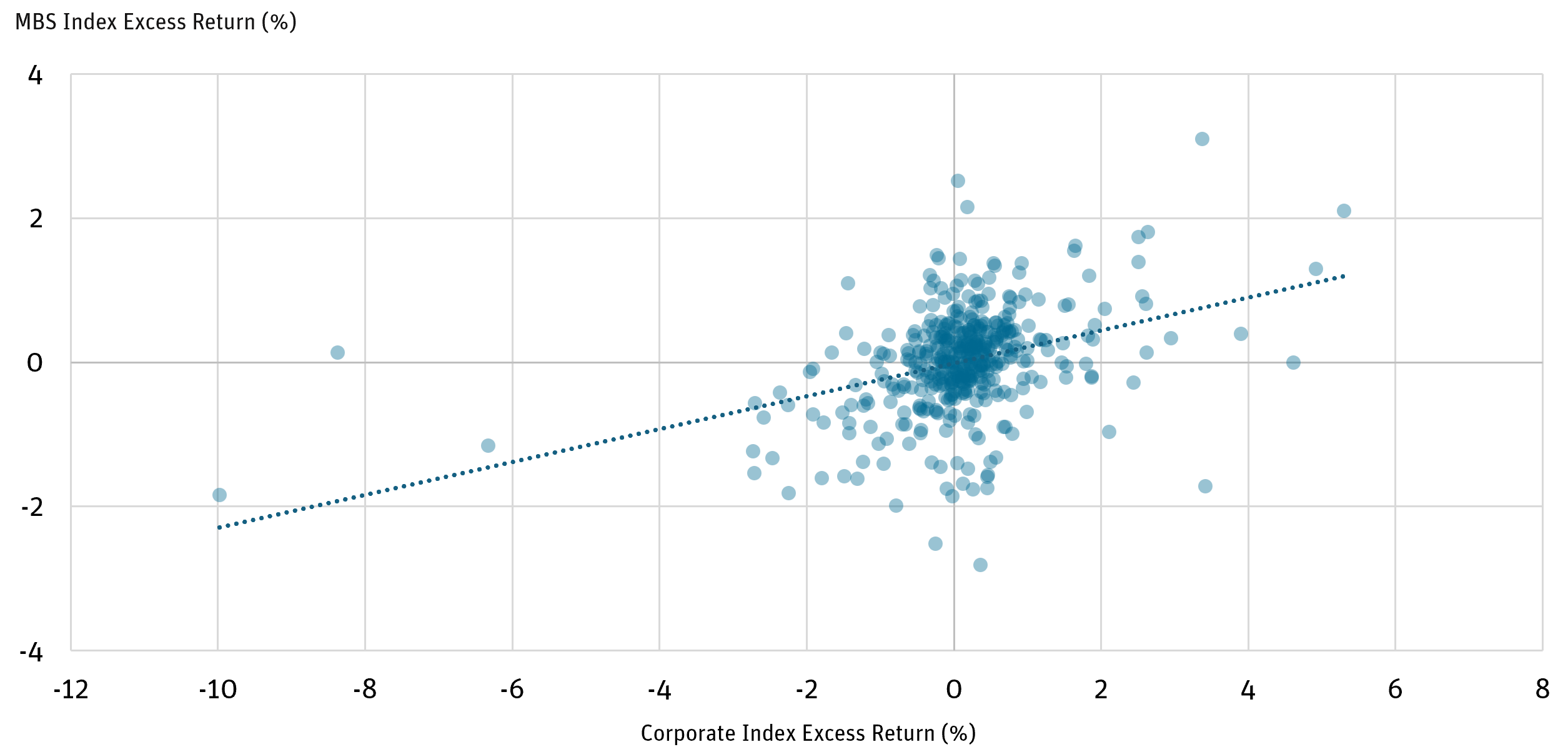

MBS offer a return profile that is meaningfully differentiated from corporate credit. Investment-grade (IG) and high-yield (HY) bonds tend to exhibit high correlations, especially during broader credit cycles (Figure 3). In contrast, MBS returns are less correlated with corporate credit (Figure 4).

This low correlation makes mortgages a compelling diversifier within fixed income portfolios. However, the prolonged period of low interest rate volatility suppressed mortgage alpha, leading many investors to underweight the sector and concentrate risk in corporate credit.

Figure 3: IG and HY Returns Are Highly Correlated (R² = 0.71)

Source: Bloomberg as of 4/30/26.

Figure 4: MBS Provide Diversification vs. Corporates (R² = 0.14)

Source: Bloomberg as of 4/30/26.

VOLATILITY CREATES AN OPPORTUNITY

With volatility structurally higher and mortgage alpha reemerging, investors have an opportunity to rebalance portfolios by adding a large, liquid, and historically uncorrelated segment of fixed income—without sacrificing return potential.

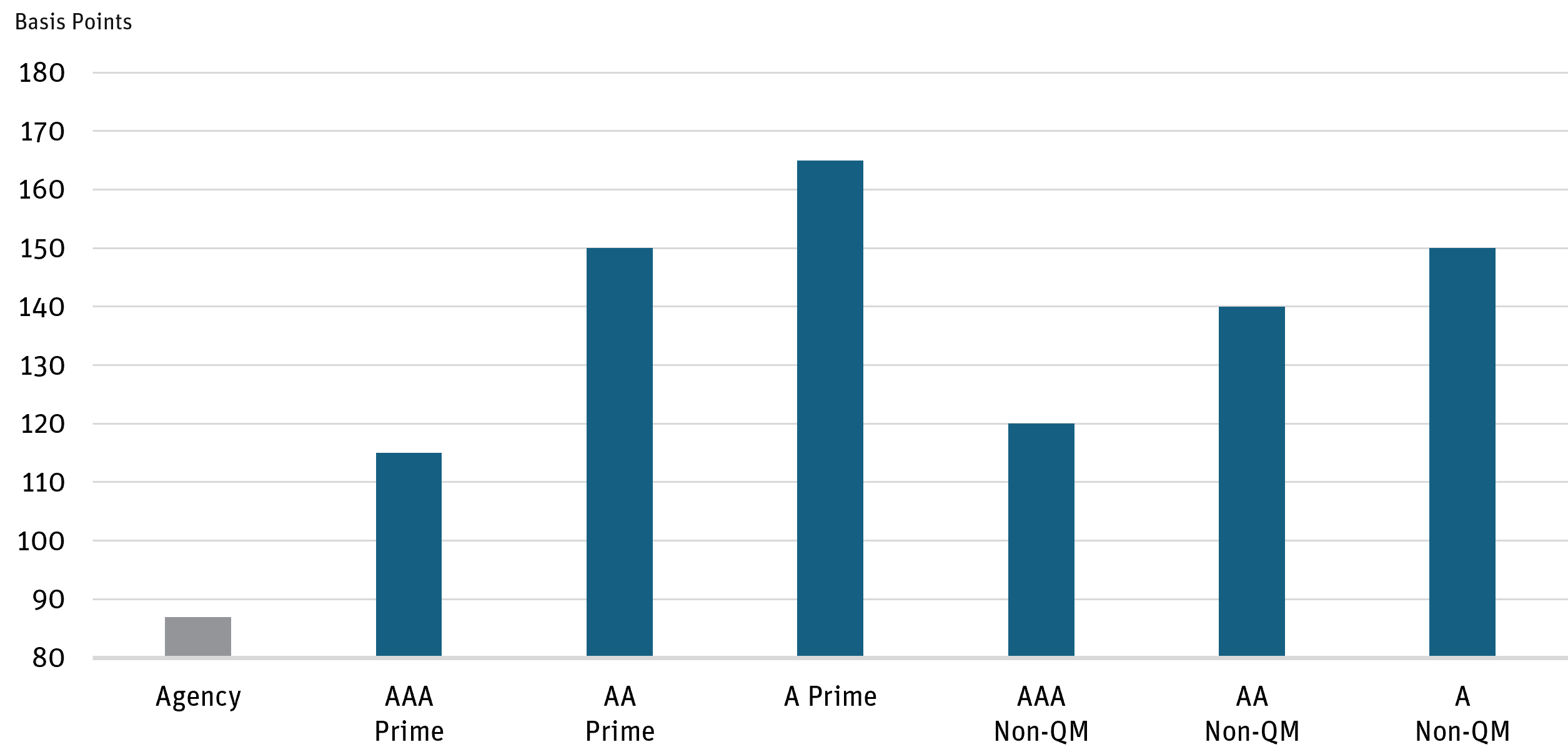

Reallocating toward mortgages can reduce reliance on corporate credit beta while enhancing diversification and potential excess returns. Investors can further improve outcomes by complementing agency RMBS exposure with higher-yielding segments of the residential mortgage market.

Prime jumbo RMBS and non-qualified mortgages provide attractive yield premiums (Figure 5) while maintaining directional alignment with agency RMBS performance. Together, these sectors offer both diversification benefits and enhanced return potential.

Figure 5: Non-Agency RMBS Offer Significant Spread Premiums

Source: BofA and Wells Fargo Securitized Products Spread History as of 5/31/26.

CONCLUSION

We believe fixed income investors should consider increasing their allocation to MBS relative to historical levels. The prolonged period of subdued interest rate volatility has given way to a more elevated and dynamic environment, enhancing the relative attractiveness of RMBS and creating the potential for incremental returns. In addition, mortgages continue to offer a liquid and differentiated source of income that remains underrepresented in many portfolios.

DEFINITIONS AND DISCLOSURES

Agency: Refers to securities, either direct debt obligations or pools of mortgage loans, that are issued or guaranteed by government-sponsored enterprises like Fannie Mae, Freddie Mac, or Ginnie Mae.

Alpha: Measures the difference between a fund’s actual returns and its expected performance, given its level of risk (as measured by beta). A positive alpha figure indicates the fund has performed better than its beta would predict. In contrast, a negative alpha indicates the fund has underperformed, given the expectations established by the fund’s beta.

Basis Point (bps): One hundredth of one percent and is used to denote the percentage change in a financial instrument.

Beta: A measure of a stock’s risk of volatility compared to the overall market.

Bloomberg U.S. Mortgage-Backed Securities (MBS) Index: An index that tracks fixed-rate agency mortgage-backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC).

Bloomberg U.S. Treasury Index: An index that covers the public obligations of the U.S. Treasury with a remaining maturity of one year or more.

Convexity: A measure of the yield curve in the relationship between a bond’s price and a bond’s yield.

Duration: Measures a portfolio’s sensitivity to changes in interest rates. Generally, the longer the duration, the greater the price change relative to interest rate movements.

ICE BofA MOVE Index: An index that measures the implied volatility of U.S. Treasury options across various maturities.

Mortgage-Backed Security (MBS): A type of asset-backed security which is secured by a mortgage or collection of mortgages.

Non-Agency: Mortgage-backed securities issued by private institutions that are not backed by government-sponsored enterprises or the U.S. Treasury.

Non-Qualified Mortgage (Non-QM): A loan that does not meet the standards of a qualified mortgage and uses non-traditional methods of income verification to help a borrower get approved for a home loan.

Option-Adjusted Spread (OAS): The yield spread which has to be added to a benchmark yield curve to discount a security’s payments to match its market price, using a dynamic pricing model that accounts for embedded options.

Prime Jumbo (PJ): Prime jumbo mortgages are non-agency loans typically because the lending amount exceeds the conforming loan limits. These tend to be high-quality mortgages with high credit scores that, for the most part, comply with agency mortgage underwriting guidelines.

Quantitative Easing (QE): A form of monetary policy in which a central bank purchases securities in the open market to reduce interest rates and increase the money supply.

R-Squared (R²): The proportion of variance in the outcome that is explained by the model.

Residential Mortgage-Backed Securities (RMBS): Fixed income securities with cash flows that are collateralized by residential mortgages.

Opinions expressed are as of 5/31/26 and are subject to change at any time, are not guaranteed, and should not be considered investment advice.

Investing involves risk; principal loss is possible. Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and nonrated securities present a greater risk of loss to principal and interest than do higher-rated securities. Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware of, including credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Derivatives involve risks different from — and in certain cases, greater than — the risks presented by more traditional investments. Derivatives may involve certain costs and risks such as illiquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lead to losses that are greater than the amount invested. The Fund may make short sales of securities, which involves the risk that losses may exceed the original amount invested. The Fund may use leverage, which may exaggerate the effect of any increase or decrease in the value of securities in the Fund’s portfolio or the Fund’s net asset value, and therefore may increase the volatility of the Fund. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are increased for emerging markets. Investments in fixed-income instruments typically decrease in value when interest rates rise. The Fund will incur higher and duplicative costs when it invests in mutual funds, ETFs, and other investment companies. There is also the risk that the Fund may suffer losses due to the investment practices of the underlying funds. For more information on these risks and other risks of the Fund, please see the Prospectus.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Angel Oak Funds. This and other important information about each Fund is contained in the Prospectus or Summary Prospectus for each Fund, which can be obtained by calling 855-751-4324 or by visiting www.angeloakcapital.com. The Prospectus or Summary Prospectus should be read carefully before investing.

Past performance does not guarantee future results.

The Angel Oak Funds are distributed by Quasar Distributors, LLC.

© 2026 Angel Oak Capital Advisors, which is the adviser to the Angel Oak Funds.