On April 30, 2026, the NAIC Life Risk-Based Capital (E) Working Group (Life RBC WG) voted to reduce the C-1 risk-based capital (RBC) factor to 0.68% for life insurance companies investing in performing residential mortgage loans (RMLs) through unaffiliated joint ventures (JVs), partnerships, or limited liability companies (LLCs). Schedule B investments in performing RMLs have long benefited from an attractive RBC charge of 0.68%. The new NAIC change can provide similar capital treatment without the need for loan-level reporting, subject to certain qualifying factors.

This development reflects a substance-over-form approach, allowing a 0.68% RBC factor regardless of investment structure. For Schedule BA funds or vehicles, reporting would consist of a single line item, with a 0.68% RBC factor applied to mortgage loans in good standing (defined as less than 90 days delinquent). The Schedule BA vehicle would need a mechanism to identify and remove loans that are more than 90 days delinquent in order to maintain eligibility for the 0.68% RBC factor. This requirement underscores the importance of active portfolio management and disciplined delinquency mitigation within a fund or strategy dedicated to this asset class.

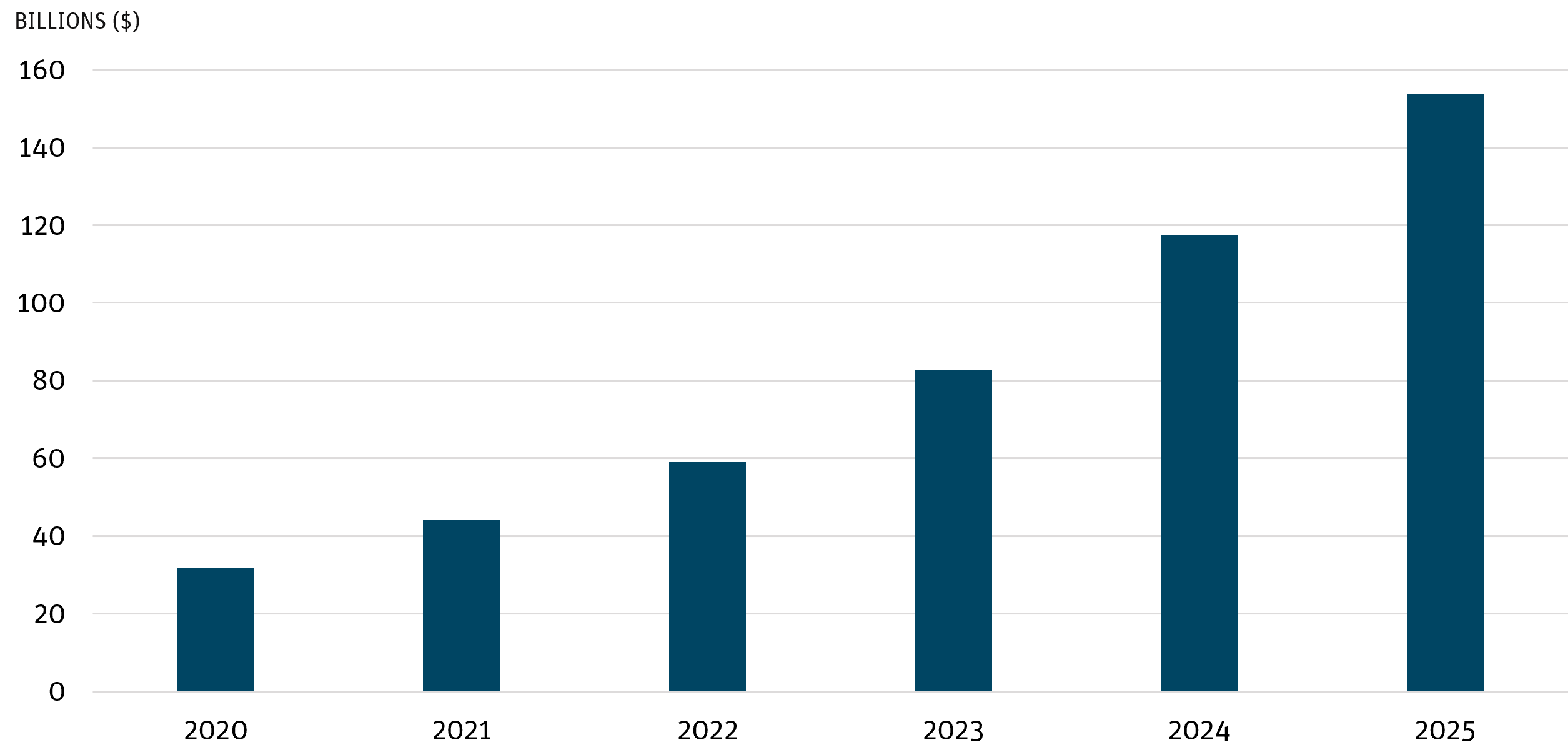

The adoption of this proposal comes at a time when life insurers have been increasing their exposure to the asset class, driven by favorable risk-adjusted yields and attractive capital treatment within general account portfolios. RML holdings have grown to over $150 billion, and according to Bank of America research, insurers purchased approximately $60 billion of RMLs in 2025.

Life Insurance Company RML Holdings

Source: NAIC, S&P Global as of 12/31/25.

Currently, the top 10 life insurance companies account for approximately 75% of all insurance company RML investments. The NAIC’s update to the capital framework may broaden participation, making it easier for smaller and midsize insurers to access the asset class. Increased structural flexibility may enable life insurers to implement residential mortgage strategies more efficiently in support of their general account objectives.

Angel Oak continues to partner with insurers to design tailored access solutions for RML investments, including separately managed accounts, funds, and securitizations. As a vertically integrated mortgage platform with a strong track record of differentiated credit performance, Angel Oak is positioned to support insurance companies seeking to expand or introduce this asset class within their portfolios.

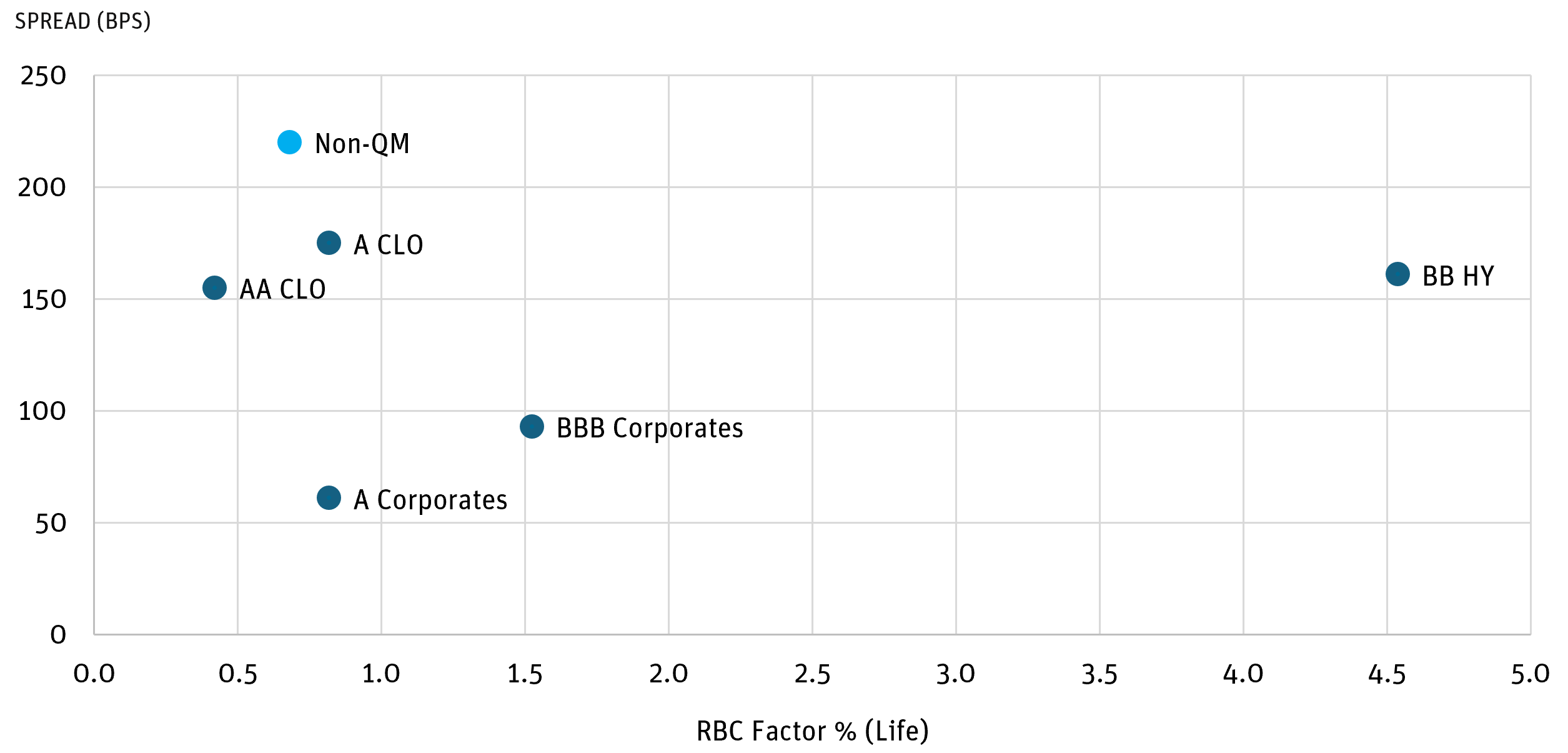

Non-Qualified Mortgage (Non-QM) Relative Value

Source: Angel Oak estimates, BofA Research as of 5/31/26.

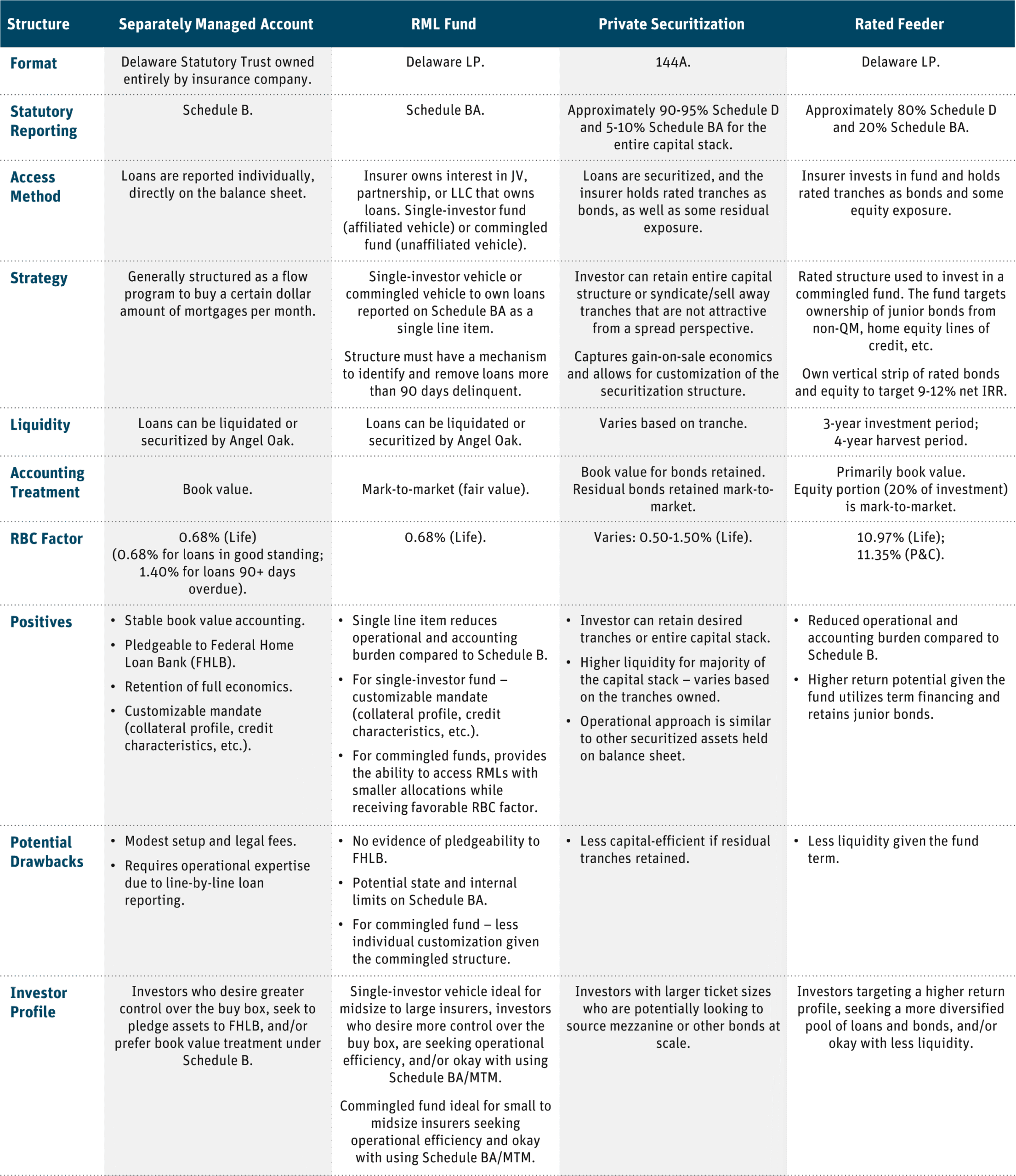

Residential Mortgage Loan Investment Structures for Insurance Companies

As of May 31, 2026

DISCLOSURES

This presentation has been prepared by Angel Oak Capital Advisors (Angel Oak or AOCA) which is solely responsible for its contents. This presentation is not intended as an offer to sell or the solicitation of an offer to buy any security. Before investing in any Strategy, an investor should carefully consider the Strategy’s investment objectives, risks, fees, and expenses. This presentation is for informational purposes only, does not constitute investment advice, and no investment decision should be made solely based on the information provided in this presentation.

Information provided reflects AOCA’s views as of a particular time. Such views are subject to change at any point without notice or update. This presentation contains forward-looking statements based on the experience and expectations of affiliates of AOCA. Such forward-looking statements are not guarantees of future performance and are subject to many risks, uncertainties and assumptions that are difficult to predict. Therefore, actual results could differ materially and adversely from those expressed or implied in any forward-looking statements as a result of various factors.

The document is being provided to you on a confidential basis and may not be re-produced or distributed without written consent from Angel Oak. By its acceptance hereof, each recipient of this presentation agrees that neither it nor its agents, representatives, directors, or employees will copy, reproduce, or distribute to others this presentation, in whole or in part, at any time without the prior written consent of AOCA and that it will keep permanently confidential information contained herein or otherwise obtained from AOCA.

Angel Oak believes the information presented herein to be reliable; however, no warranty or guarantee is made as to its accuracy or completeness. Data has been obtained from reliable sources; however, Angel Oak cannot be responsible for errors or omissions from such sources.

These investment strategies are speculative and involve substantial risks, including the risk of loss of an investor’s entire investment, which an investor should be willing to accept. No assurance can be given that profits will be achieved or that losses will not be incurred. Client losses may be incurred due to declines in one or more markets in which a Client invests. These declines may be the result of, among other things, political, regulatory, market, economic, or social developments affecting the relevant market(s). In addition, turbulence and reduced liquidity in financial markets may negatively affect many issuers, which could have an adverse effect on a Client’s investment. Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and nonrated securities present a greater risk of loss to principal and interest than higher-rated securities do. Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware of, including credit risk, prepayment risk, possible illiquidity, and default, as well as increased susceptibility to adverse economic developments. Derivatives involve risks different from—and in certain cases, greater than—the risks presented by more traditional investments. Derivatives may involve certain costs and risks such as illiquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Investing in derivatives could lead to losses that are greater than the amount invested.

Past performance is no guarantee of future returns. No guarantee of investment performance is being provided and no inference to the contrary should be made.