ATLANTA — (June 18, 2025) — Angel Oak Financial Strategies Income Term Trust (NYSE: FINS) (the “Fund”) is pleased to share an update on the Fund’s capital deployment and general performance following the successful completion of its recent rights offering, which was significantly oversubscribed and raised approximately $110.4 million in gross proceeds. Strong demand drove the oversubscription, with robust participation from existing shareholders, which the Fund believes reflects their confidence in the Fund’s management team and investment strategy.

For the period ended May 31, 2025, FINS has outperformed its index on a 1-year, 3-year, 5-year and since-inception basis. Additionally, FINS pays out a distribution of over 10% and has narrowed its discount to 5.6% as of May 31, 2025, one of the largest improvements of its peer group over the past year. The Fund’s management team continues to deploy fresh capital into higher-coupon bank debt, taking advantage of the marked increase in issuance volumes, as community and regional banks seek to refinance or call debt originated during the post-COVID 2020 vintage.

“The banking sector has several notable tailwinds we are seeking to take advantage of, given strong credit fundamentals across the banking system, with expanding net interest margins, stable credit quality and a growing pipeline of M&A activity,” said Johannes Palsson, Portfolio Manager for the Fund. “The success of our recent offering validates our conviction in the opportunities we’re seeing across the financial sector, and we look forward to deploying capital in the current environment.”

“With decades of experience across our management team and nearly $2 billion invested across private and public strategies in regional and community bank debt, Angel Oak is well positioned to deploy capital and deliver value for our investors,” said Sreeni Prabhu, Managing Partner and Group Chief Investment Officer. “Our success in managing through multiple cycles and our established presence in the bank-debt sector for more than a decade bode well for the bullish outlook we expect to maintain over the next six to 12 months.”

NAV PERFORMANCE AND THE RIGHTS OFFERING

Ahead of the rights offering share issuance, FINS’ 2025 year-to-date NAV performance benefitted from the resumption of bank debt primary market issuance with meaningful volume, following a slowdown in 2023 and early 2024 due to rising interest rates and the lingering effects of the regional banking crisis. New investment-grade bank debt is coming to market at highly attractive coupons, and pricing has improved on legacy portfolio positions. Notably, a significant portion of the legacy bank-debt portfolio is approaching its call and floating-rate period within the next 12 months, which the Fund believes will position these holdings to pull to par as deals reset to floating rate or are called. Additionally, select tactical equity positions rebounded sharply post-Liberation Day. Tactical opportunities remain a small portion of the Fund, accounting for less than 10% of overall AUM as of May 31, 2025.

During the recent rights offering period, NAV was affected by heightened volatility surrounding two specific equity and preferred equity positions: KINS and PNBK.

- KINS: Angel Oak received warrants with a $1 strike price in conjunction with KINS’s 2022 bond issuance. The company reported strong quarterly earnings and is slated for inclusion in the Russell 3000 on June 27, 2025. While the stock initially rallied following earnings, it has since pulled back over the past month. The position remains well in the money and the Fund believes it continues to offer an attractive risk-reward profile.

- PNBK: Following a recapitalization under new management in March 2025—including new common and convertible preferred equity — PNBK’s stock performance ahead of the lockup expiration exceeded expectations by several standard deviations before returning to a more normalized valuation post-expiration. This position also remains well in the money and the Fund believes it is attractive from a risk-reward standpoint.

Following the close of the recent rights offering, Angel Oak’s investment team rapidly deployed proceeds into money center and regional bank debt to eliminate cash drag. As the issuance calendar accelerates, the team continues to optimize the portfolio by adding higher-coupon community bank bonds. Approximately one-third of the proceeds have already been redeployed, with an average coupon of 7.65% on new community bank-debt investments (range: 7.00%-8.50%), which is over 100 basis points higher than the Fund’s average coupon of 6.49% as of March 31, 2025. The team believes the near-term pipeline remains strong, with anticipated new issue coupons ranging from 7.50% to 8.75%.

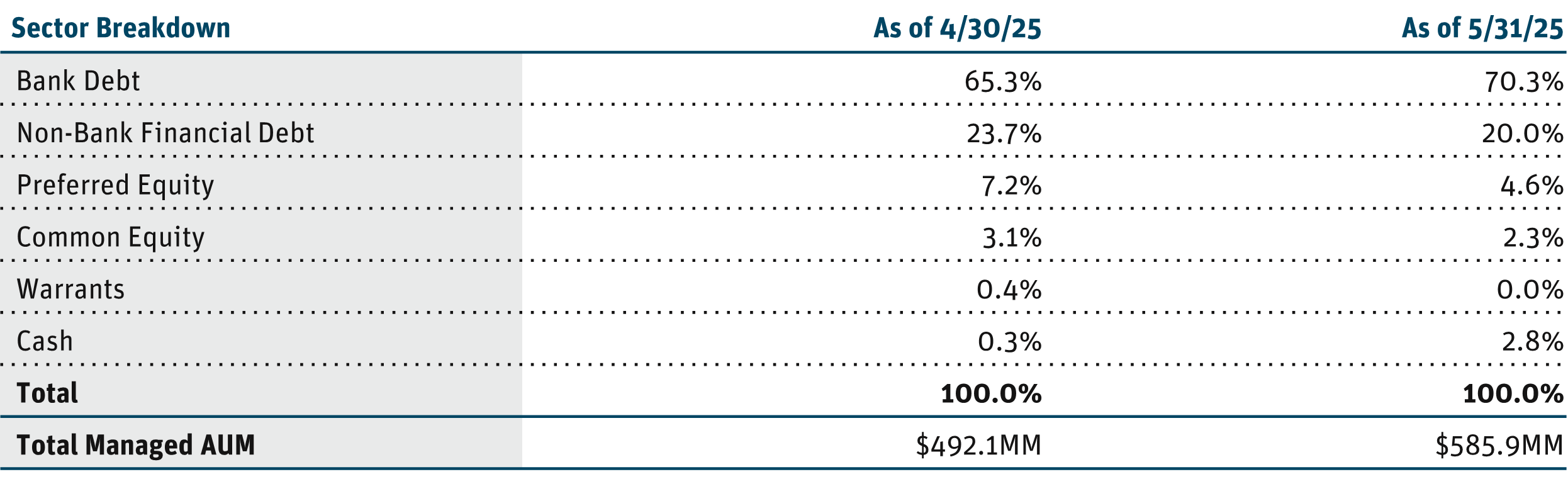

SECTOR AND AUM BREAKDOWN

HOLDINGS

Click here to access the Fund’s holdings as of 4/30/25.

Click here to access the Fund’s holdings as of 5/31/25.

ABOUT FINS

Led by Angel Oak’s experienced financial services team, FINS invests predominantly in U.S. financial sector debt as well as selective opportunities across financial sector preferred and common equity. Under normal circumstances, at least 50% of FINS’ portfolio is publicly rated investment grade or, if unrated, judged to be of investment grade quality by Angel Oak.

ABOUT ANGEL OAK CAPITAL ADVISORS, LLC

Angel Oak Capital Advisors (the “Adviser”) is an investment management firm focused on providing compelling fixed-income investment solutions to its clients. Backed by a value-driven approach, the Adviser seeks to deliver attractive, risk-adjusted returns through a combination of stable current income and price appreciation. Its experienced investment team seeks the best opportunities in fixed income, with a specialization in mortgage-backed securities and other areas of structured credit.

On April 1, 2025, Angel Oak Companies, LP, the parent of Angel Oak Asset Management Holdings, LLC, itself the parent company of the Adviser, announced that it signed a definitive agreement pursuant to which Brookfield Asset Management Ltd. will acquire a majority interest in Angel Oak Companies, LP and its subsidiaries, including the Adviser (the “Transaction”). The closing of the Transaction is expected to be completed by September 30, 2025. The Transaction is not expected to result in any material change in the day-to-day management of the Fund. However, the closing of the Transaction is subject to certain conditions, and there can be no assurance that the Transaction will be completed as planned, or that the necessary conditions will be satisfied. If successful, the closing of the Transaction would be deemed to be a change of “control” of Angel Oak Companies, LP and its subsidiaries (collectively, “Angel Oak”), including the Adviser, under the Investment Company Act of 1940, and deemed “assignment” of the Fund’s investment advisory agreement (the “Existing Advisory Agreement”), which would result in the automatic termination of the Fund’s Existing Advisory Agreement. However, following the closing of the Transaction, the existing management team of Angel Oak will continue to independently manage the day-to-day business of Angel Oak and the Adviser, and will control the board of directors of Angel Oak.

At a meeting held on April 23, 2025, the Board of the Fund approved a new investment advisory agreement between Angel Oak and the Fund (the “New Advisory Agreement”), subject to shareholder approval at a shareholder meeting to be held on June 26, 2025. This communication is not a proxy and is not soliciting any proxy in connection therewith, which can only be done by means of a proxy statement.

Information regarding the Fund and Angel Oak Capital Advisors can be found at www.angeloakcapital.com.

Past performance is neither indicative nor a guarantee of future results. Investors should read the prospectus supplement and accompanying prospectus and consider the investment objective and policies, risk considerations, charges and ongoing expenses of an investment carefully before investing. For more information, please contact your investment representative or EQ Fund Solutions at 866.751.6314.