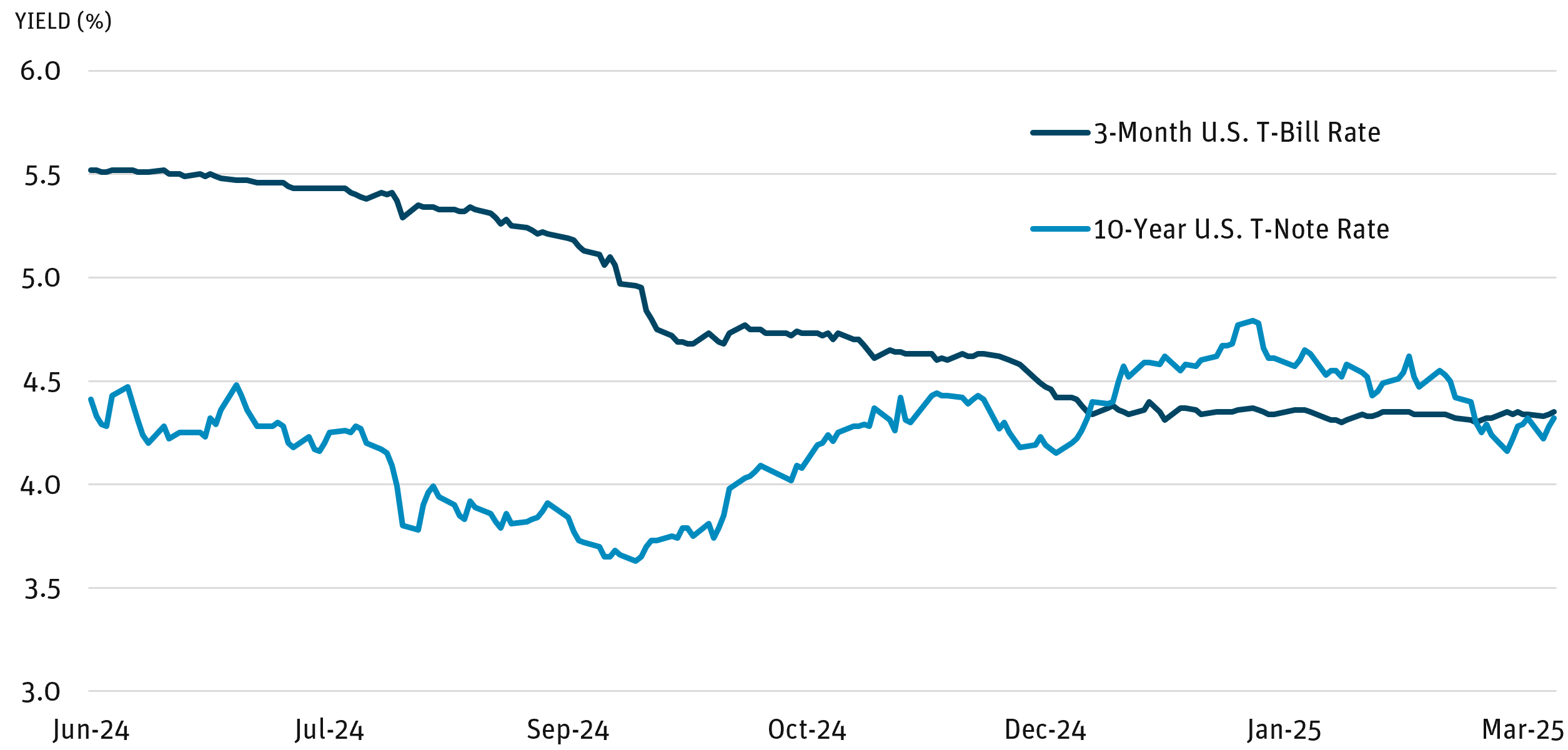

Angel Oak recommends reducing exposures to floating rate positions and extending duration in advance of potential Federal Open Market Committee (FOMC) policy cuts. Investors who retreated into cash/money markets during the 2022-23 rate-hiking cycle had been earning risk-free yields of 5% or more. However, U.S. Treasury bill yields (a proxy for money market rates) were trending downward even prior to the FOMC cuts in September 2024, while longer-term U.S. T-note rates have been trending upward as the slope of the yield curve has become more “normal” (Figure 1).

Figure 1: U.S. Treasury Rates

Source: Bloomberg as of 3/12/25.

Although many factors underpin the strength of the U.S. economy, there are also signals suggesting a higher probability of slowing growth. Recent data reflect increasing uncertainty regarding U.S. trade policies from the incoming administration. The Nasdaq and S&P indices entered correction territory (a 10% drop from recent highs), and other equity market indices were broadly lower as of early March 2025.

Despite this, disinflation appears to be on track while labor markets remain solid. The February Consumer Price Index rose 2.8% year over year, beating market expectations (Figure 2). Nonfarm payrolls increased by 151,000 in February, in line with the average monthly gain of 168,000 over the prior 12 months.

Figure 2: U.S. Consumer Price Indices

Source: Federal Reserve as of 2/28/25.

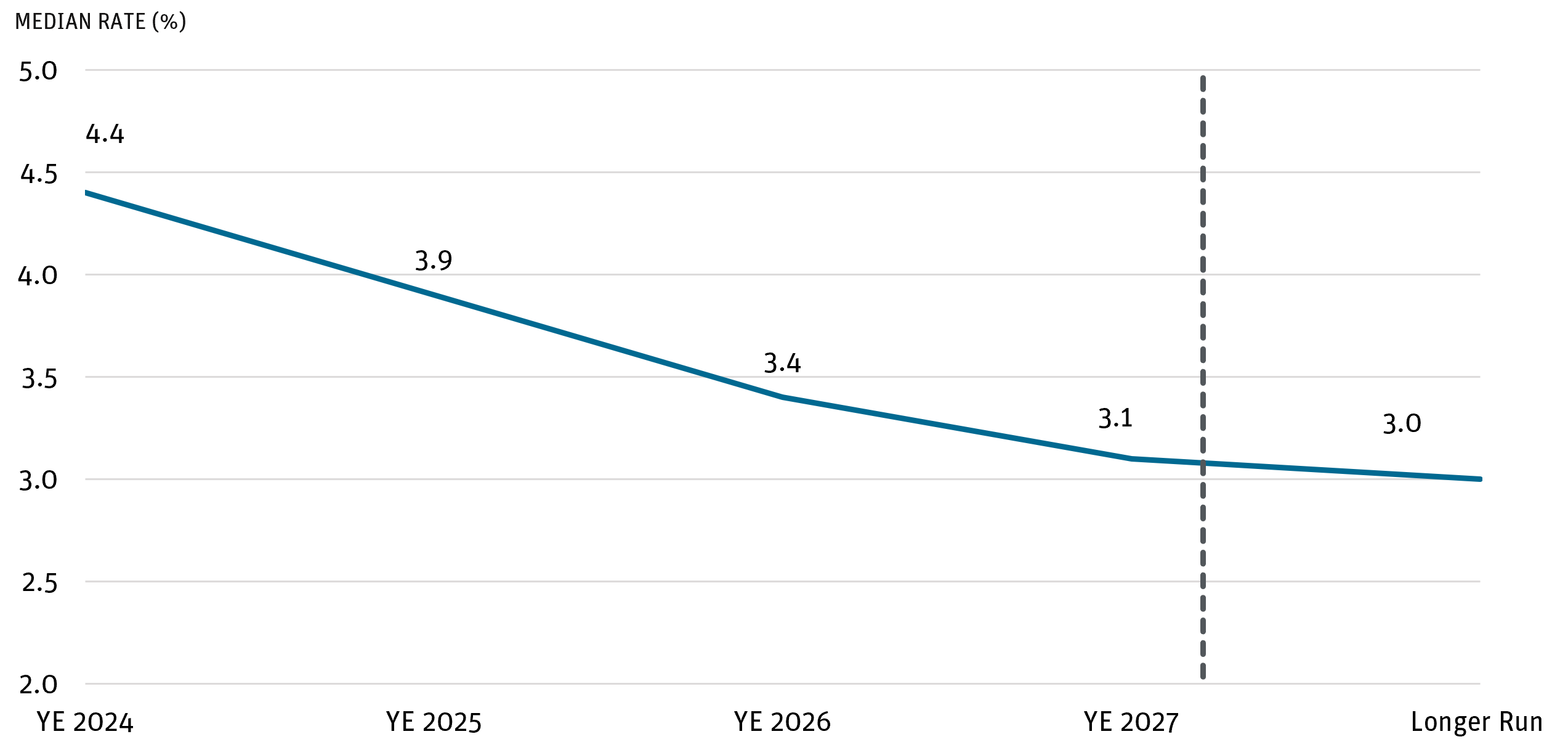

Fed Chair Jay Powell recently stated that “despite elevated levels of uncertainty, the U.S. economy continues to be in a good place.” After lowering the federal funds target rate by 50 basis points in the third quarter, subsequent FOMC meetings (including the recent March 18-19 meeting) have not resulted in additional rate cuts. However, projections for 2025 and beyond suggest that the Fed believes further cuts will be necessary to ensure strong labor markets without excessive inflation (Figure 3).

Figure 3: FOMC Summary of Economic Projections for Fed Funds Rate

Source: Federal Reserve as of 3/19/25.

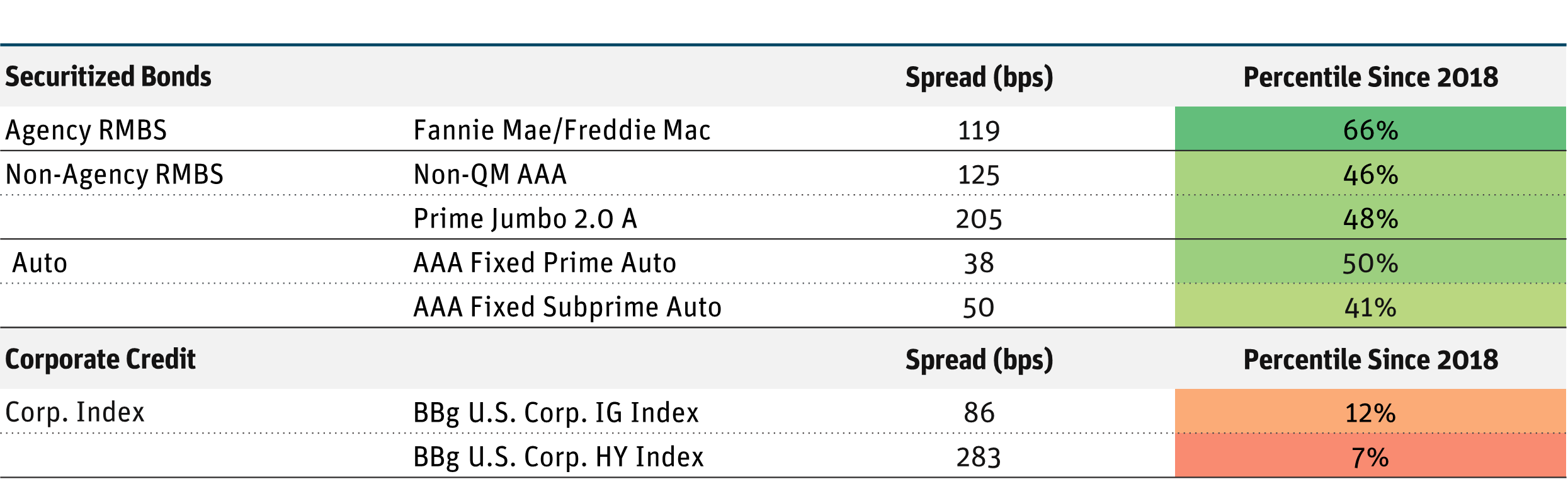

With markets currently pricing in approximately three additional cuts in 2025 based on decreasing growth expectations, high-quality fixed income portfolios of intermediate duration have the potential to mitigate reinvestment risk and generate total returns that are greater than current yields. While corporate credit valuations appear rich, securitized bonds still have room to run (Figure 4).

Figure 4: Historical Spreads of Fixed Income Bonds

Source: Bloomberg, Wells Fargo, Bank of America as of 2/28/25.

We believe this is an opportune time for investors to lock in today’s favorable yield levels and potential for greater price appreciation. We recommend a shift from cash/money market allocations into intermediate-term fixed-income positions with a focus on high-quality securitized bonds.

DEFINITIONS AND DISCLOSURES

Basis Point (bps): One hundredth of one percent and is used to denote the percentage change in a financial instrument.

Bloomberg U.S. Aggregate Bond Index: An unmanaged index that measures the performance of the investment-grade universe of bonds issued in the United States. The index includes institutionally traded U.S. Treasury, government sponsored, mortgage and corporate securities.

Bloomberg U.S. 1-3 Month Treasury Bill Index: : Measures the performance of public obligations of the U.S. Treasury that have a remaining maturity of greater than or equal to 1 month and less than 3 months.

Consumer Price Index (CPI): An index that measures the changes in the price of a certain collection of goods and services bought by consumers in an effort to measure inflation.

Current Coupon: Refers to a security that is trading closest to its par value without going over par. In other words, the bond’s market price is at or near to its issued face value.

Duration: Measures a portfolio’s sensitivity to changes in interest rates. Generally, the longer the duration, the greater the price change relative to interest rate movements.

Federal Funds Target Rate: A target interest rate set by the central bank in its efforts to influence short-term interest rates as part of its monetary policy strategy.

Floating Rate: A floating-rate security is an investment with interest payments that float or adjust periodically based upon a predetermined benchmark.

FOMC Dot Plot: A chart summarizing the Federal Open Market Committee’s outlook for the federal funds rate. Each dot marks where a respective FOMC member expects the federal funds rate to be at the end of a particular period.

Spread: The difference in yield between a U.S. Treasury bond and a debt security with the same maturity but of lesser quality.

Yield Curve: The U.S. Treasury yield curve refers to a line chart that depicts the yields of short-term Treasury bills compared to the yields of long-term Treasury notes and bonds.

Opinions expressed are as of 3/19/25 and are subject to change at any time, are not guaranteed, and should not be considered investment advice.

Investing involves risk; principal loss is possible. Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and nonrated securities present a greater risk of loss to principal and interest than do higher-rated securities. Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware of, including credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Derivatives involve risks different from — and in certain cases, greater than — the risks presented by more traditional investments. Derivatives may involve certain costs and risks such as illiquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lead to losses that are greater than the amount invested. The Fund may make short sales of securities, which involves the risk that losses may exceed the original amount invested. The Fund may use leverage, which may exaggerate the effect of any increase or decrease in the value of securities in the Fund’s portfolio or the Fund’s net asset value, and therefore may increase the volatility of the Fund. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are increased for emerging markets. Investments in fixed-income instruments typically decrease in value when interest rates rise. The Fund will incur higher and duplicative costs when it invests in mutual funds, ETFs and other investment companies. There is also the risk that the Fund may suffer losses due to the investment practices of the underlying funds. For more information on these risks and other risks of the Fund, please see the Prospectus.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Angel Oak Funds. This and other important information about each Fund is contained in the Prospectus or Summary Prospectus for each Fund, which can be obtained by calling 855-751-4324 or by visiting www.angeloakcapital.com. The Prospectus or Summary Prospectus should be read carefully before investing.

Index performance is not indicative of Fund performance. Past performance does not guarantee future results. Current performance can be obtained by calling 855-751- 4324.

The Angel Oak Funds are distributed by Quasar Distributors, LLC.

© 2025 Angel Oak Capital Advisors, which is the adviser to the Angel Oak Funds.